Diligence is Vigilance

The final article in a series about how biopharma BD&L should use the patent record in a post-FOIA world.

One observation that has held up across three decades of biopharma BD&L: the diligence that protects a deal is not the diligence done in the data room. It is the diligence done afterward, quarterly in alliance committee meetings and repeatedly, against an IP record that keeps changing. The data-room version is a snapshot — the spec, the family chart, the prior-art search — taken once, with the deal as the deadline. The vigilance version is what the patent counsel and the BD&L team continue to do for the ten or fifteen years over which the asset’s value actually accrues, watching the prosecution, the oppositions, the third-party filings, the family extensions, and the appeals in the jurisdictions that matter. The deal negotiation closes on the snapshot. The asset survives, or doesn’t, on the vigilance.

What is different post-FOIA is that the patent record is now the primary surface on which both the snapshot and the vigilance can be read by a prospective counterparty. What survived 2020 is the record of what happens to a patent once it is filed: every office action, every continuation-in-part (CIP), every opposition in the European Patent Office (EPO), every Inter Partes Review (IPR) before the Patent Trial and Appeal Board (PTAB), every assignment recorded with the USPTO, every appeal round in Japan, India, or Brazil. It is work performed in the open against a docket — and a counterparty’s behavior in front of an examiner or an opposer is not a press release.

TL1A — the TNF-family ligand whose neutralization is now the landscape in next-generation inflammatory bowel disease (IBD) — is a useful place to read this directly. In April 2023, Merck (MSD) acquired Prometheus Biosciences for approximately $10.8 billion, in a transaction whose only material asset was the anti-TL1A antibody PRA023, since renamed tulisokibart (MK-7240). In October 2023, Pfizer acquired the Telavant subsidiary from Roivant Sciences for approximately $7.1 billion, whose only material asset was the anti-TL1A antibody RVT-3101 (now afimkibart, PF-06480605). Two of the four largest pharmaceutical-company acquisitions of 2023 were single-asset anti-TL1A deals.

Reading the spec record of those programs against a structured rubric — abstract specificity (KC1), claim-type strength (KC2), dependent fallback hierarchy (KC3), prior-art neighborhood (KC4), Amgen v. Sanofi enablement (KC5), and strategic / multi-jurisdictional breadth (KC6) — gives a sharper picture of what each acquirer actually bought than the deal announcements did. The exercise covered 260 published TL1A-related biopharma patents; the top decile distills to twenty-six, and a complete head-to-head pairwise tournament across that top decile (325 pairs) finishes with the rank #1 filing at 25 wins and 0 losses, the rank #2 at 24-1, the rank #3 at 23-2, and a clean monotonic decline from there. The top decile by assignee resolves to twelve Cedars-Sinai Medical Center filings, five Pfizer / BMS-joint filings (some predating the Roivant arc, one Pfizer-solo continuation from 2024), four Teva filings on the original C320 DR3-selective lineage, two Amgen anti-TL1A / anti-TNFα bispecific filings, one Prometheus filing (which holds the rank #1 position), one Cephalon / Teva filing on the duvakitug parent (TEV-48574, the program Sanofi co-develops), and one filing each from Paragon Therapeutics and a small group of academic and emerging filers.

The Cedars-Sinai pattern is the cleanest illustration. The foundational humanized anti-TL1A composition US 11,292,848 traces to a 2019 priority date, prosecutes against the IGHV1-46*02 / IGKV3-20 framework on which tulisokibart is built, and finishes the tournament at calibrated rank #2 with a 24-1 record. Its granted continuation US 11,999,789 sits at rank #3 (23-2), and four further Cedars-Sinai humanization-family publications populate ranks #4, #5, #8, and #9. Prometheus in-licensed that foundational position, prosecuted around it, and added the rank #1 filing in the IP landscape — a Predictive Response Index (PRI) companion-diagnostic specification that ties the anti-TL1A treatment to a quantitatively defined patient-selection algorithm with PPV ≥29% and 747 total claims. What Merck acquired was not a single antibody but a foundational composition layer of academic origin, a continuing prosecution arc managed jointly with the academic licensor, and a companion-diagnostic claim layer that converts the program from an antibody asset into a precision-IBD platform. None of that is observable from the deal announcement.

The Pfizer pattern is a different version of the same thesis. The granted Pfizer / BMS-joint US 9,683,998 — the parental-clone composition (1D1, 7D4, 26B11) from which RVT-3101 / PF-06480605 was developed during the Roivant period — sits at calibrated rank #6 with a 20-5 tournament record and includes a co-crystal structure of three 1D1 scFv with the TL1A trimer that defines the DR3-blocking epitope. The 2018 publication of the affinity-matured 1D1 1.31 variant follows at rank #7 (19-6); the original 2015 publication of the same family, predating Pfizer’s eventual sole control of the asset, sits at rank #12. When Pfizer acquired Telavant, the parental-clone composition layer was not new IP to integrate; it was IP Pfizer had been prosecuting jointly with BMS for the better part of a decade, with crystal-structure-defined epitope coverage in force since 2017. Read on the patent record, the Telavant transaction is less a discontinuity than a re-internalization. The Cephalon / Teva line is a third pattern: Teva’s continuing prosecution of the parental 320-179 antibody — affinity-matured variants with 10-to-40-fold potency gains and dual DR3 / DcR3 binding — sits at calibrated rank #10 in the form of the duvakitug parent US20220185902A1 (TEV-48574, co-developed with Sanofi, with positive Phase 2b UC and CD readouts in 2024). Teva’s earlier and structurally distinct C320 DR3-selective program contributes four further top-decile filings at ranks #14 through #17 and #21. The patent record records what work has been performed; it does not care which company is in commercial favor.

Two further patterns are worth naming. Amgen’s anti-TL1A / anti-TNFα bispecific — granted 2026 as US 12,552,877 with its 2022 publication immediately behind it — sits at calibrated ranks #18 and #19, the only dual-target TL1A architecture in the top decile and a structurally novel format hetero-IgG with charge-pair mutations and IgG-Fab tetravalent constructs. It is, on the patent record, the first-in-class incumbent on a different mechanism class within the same target — a pattern this series last read in the KRAS analysis, where the chemically distinct fast follower’s foundational composition layer outranked the launchers’ lifecycle and process IP. Paragon Therapeutics’ US 12,509,523 — granted in late 2025 and explicitly differentiated against RVT-3101, MK-7240, and TEV-48574 in its specification — sits at calibrated rank #26, the bottom of the top decile, finishing the tournament at 0-25. The fast follower whose specification names the existing clinical-stage competitors as the prior art it is distinguishing itself from is, structurally, in a different position than the foundational filers above it; the patent record records the difference even when the press-release version cannot.

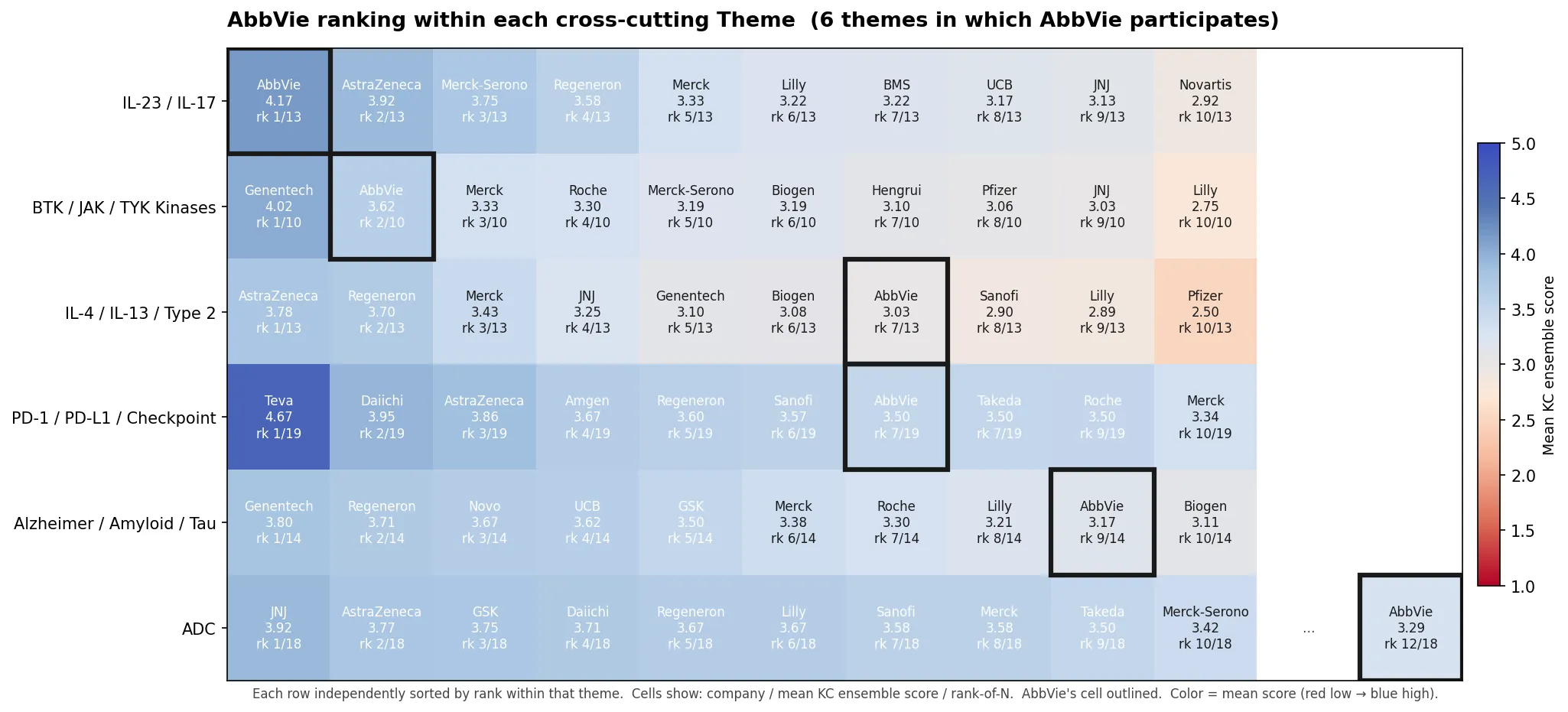

The KCs (or Key Components) are not equally informative for partner-of-choice analysis. KC1, KC2, and KC3 are largely set at filing or in early prosecution. KC4, KC5, and KC6 — prior-art neighborhood, enablement support, and multi-jurisdictional family management — are the dimensions on which a counterparty’s continuing vigilance is most legible, and they organize cleanly into a per-theme display. The exhibit below shows AbbVie’s position within each of the six cross-cutting therapeutic themes in which it participates, alongside the top comparator filers in each theme; cells are colored by mean ensemble score across KC1–KC6, with AbbVie’s cell outlined.

The heatmap display of AbbVie’s recent IP filings for selected themes answers a question the press-release version of AbbVie cannot. The IL-23 / IL-17 and BTK / JAK / TYK rows read as one would expect — Skyrizi, Rinvoq, and the broader inflammation franchise supported by foundational filing strength. The IL-4 / IL-13 / Type 2 row is more interesting: AbbVie sits at rank 7 of 13, behind AstraZeneca, Regeneron, Merck, J&J, Genentech, and Biogen, all of whom carry deeper foundational filings in that theme. The ADC row, at rank 12 of 18, reads as a participation position rather than a foundational one. None of this is an indictment; it is an honest read of where the prosecution work has been done and where it has not, and it is the kind of read a counterparty looking at a Type 2 inflammatory or ADC asset should do before walking into the conversation.

The partners worth choosing are not the partners who appear when no one else is shopping. Biopharma BD&L practitioners track the IPO market and the M&A window as well as alliance volume because a strong adjacent financing environment shifts a biotech’s preference away from alliances entirely — a robust IPO market means “let’s not do alliances for a while”; a robust M&A market means “don’t do an alliance if you could possibly do an exit.” Neither favorable environment lasts long. The partners with the patience and balance sheets to do alliances throughout the cycle are not the same partners who pile in when other windows close, and the patent record reveals the difference: prosecution depth across multiple jurisdictions, sustained third-party IP acquisition over a decade, and a track record of defending in-licensed IP through IPRs and oppositions are all observable proxies for counter-cyclical commitment. The procyclic partners can be identified by what is absent in their patent-office behavior, not by anything they project at industry conferences.

This is the line of analysis I’m pursuing now under rDNA.ai. All five articles in this series are accessible on the rdna.ai website, along with full KC-scored analyses of the epigenome editing IP (Article 2), the GLP-1 / dual-agonist / triple-agonist incretin IP (Article 3), the KRAS / RAS-pathway IP (Article 4), and the TL1A IP (Article 5).

A patent docket is, in the end, a public archive. The diligence done in the data room reads the index. The diligence done over the ten years that follow reads the catalog, the additions, the withdrawals, and the holdings the librarians decided to keep. The post-FOIA world is one in which the catalog is the only honest record of who has been doing the work — and the BD&L professionals worth working with are the ones who never stopped reading it.

This is the fifth and final article in this series on what biopharma BD&L practitioners can read from the patent record now that the FOIA-disclosed contract record has ended. Here’s the start of the series .

I’m planning to write a few more articles using an improved KC scoring methodology (V3). V3’s value over current KC scoring is in the structured Retrieval-Augmented Generation (RAG) novelty signal, the per-sub-dimension model routing, the tournament calibration of the top decile, and the patent-by-patent KC composite prompting that’s now anchored to the V2 holistic-judgment framework. Both have known limits — V3’s RAG is limited by the patent discovery collection (a true prior-art landscape would extend beyond the target-specific search into broader scientific publications), and the tournament calibrates internal consistency rather than predictive validity. The follow-on articles will show what V3 does really well.